I have one more constitutional fix for Washington State to round out the suite of sustainability amendments that should be considered in the next legislative session. (The first was a repeal or rewrite of the state’s 18th Amendment restricting the use of taxes collected on cars for highways; the second was a fix to allow the state to loan its credit for energy efficiency retrofits.) Constitutional fixes are never easy, but Tax Increment Financing (TIF) is like a double black diamond for sure. It’s been awhile since I’ve been skiing, but one thing I learned was once you’ve committed to a run you’ve gotta get down. I’ve been a pretty committed supporter of making TIF happen in Washington, so even though it’s a challenge here’s some background and my thinking on how we get started.

I have one more constitutional fix for Washington State to round out the suite of sustainability amendments that should be considered in the next legislative session. (The first was a repeal or rewrite of the state’s 18th Amendment restricting the use of taxes collected on cars for highways; the second was a fix to allow the state to loan its credit for energy efficiency retrofits.) Constitutional fixes are never easy, but Tax Increment Financing (TIF) is like a double black diamond for sure. It’s been awhile since I’ve been skiing, but one thing I learned was once you’ve committed to a run you’ve gotta get down. I’ve been a pretty committed supporter of making TIF happen in Washington, so even though it’s a challenge here’s some background and my thinking on how we get started.

Tax Increment Financing (TIF) is a financial tool that allows local governments to sell debt in the form of bonds to pay for infrastructure (roads, drainage, district energy) that would promote development in areas where those local improvements are made. Most often this means the creation of a new neighborhood district like Portland’s Peal District. Before TIF investments in the Pearl, the neighborhood was a mix of railroad tracks, warehouses, and industrial uses (a lot like Seattle’s Interbay). Now it is a compact neighborhood with excellent transit, lots of housing and retail, and a model of what smart growth should look like. So not only is TIF a good way to improve public infrastructure, it can create the kind of dense, compact growth that is more sustainable than sprawl.

And the improvements paid for by TIF increase the assessed value of the underlying properties, so the local government is able to use that incremental increase in collected tax revenue to service the debt. If the project is successful, once the debt is paid off, the various local taxing authorities get to keep that additional tax revenue. The beauty of TIF is that when it works, it allows a big boost in public benefits—increased tax revenues, better infrastructure, new housing—without local government having to spend general fund dollars.

Oregon notably has tax increment financing, which it implements through the Portland Development Commission (PDC). Washington doesn’t have it. Here’s why I think TIF is an important strategy to promoting the kind of dense, transit oriented development we need to see in Washington’s cities to support sustainability.

- Wise use of public financing—TIF reaps the benefits of improvements without having to tap into shrinking general funds;

- Improves tax base—when the bonds are retired, new revenue flows into the general fund of the local government and other taxing districts;

- Comprehensive development—TIF allows bigger projects with lots of infrastructure needs to move forward together rather than in a lot-by-lot piecemeal fashion; and

- Promotes economic development—new development can create and save good paying, career-ladder jobs in a very depressed construction sector.

Because it can use TIF, the Portland Development Commission (PDC) has the power to provide financial support for large-scale development, the kind of thing that makes Portland’s Pearl District the envy of cities throughout the country. TIF allows a local government to take an area that doesn’t support much housing and improve the infrastructure to supports lots of housing and new residents. It’s an ideal strategy for accommodating growth by building public amenities that will enable home buyers to choose living in a condominium rather than a single-family home in a far-flung community, which we should remember is serviced by ribbons of publicly subsidized highways.

So why hasn’t TIF happened in Washington? This is the double black diamond ski run I was talking about. There are some big structural and political moguls in the way.

TIF was actually considered by Washington voters 25 years ago and it failed at the ballot. Later, it was tried in Spokane without any changes to the law, but that effort was ruled unconstitutional based on the Washington State Supreme Court’s determination (Leonard v. Spokane, 1995) that TIF would violate Article IX of the Washington State Constitution.

Article IX is the portion of the constitution that determines that the paramount duty of the state is educating children. The conflict arises because Article IX currently requires that a portion of the increased tax revenue generated from the TIF-funded improvements would go to pay for education. In fact, there is a “state school tax,” which is a property tax assessed specifically for the benefit of public education. But in order for TIF to work, the increased revenue would not at first go to the state school tax, but to retiring the TIF-related debt. And Washington courts (see especially the Doran decision) have consistently held that the state’s paramount duty is more than aspirational, it means that education has to be fully funded.

Because TIF directs the increased tax revenue to retire the debt on the TIF bonds, the court found that it would be a diversion of funds away from schools, making it a violation of Article IX and the basic premise of the Doran decision. So, in order for full TIF to work in Washington—in which all the increased incremental value in tax revenue from multiple taxing districts is used for debt service—some portion of the state school tax would have to be used to pay off the bonds. The Court ruled that this was a diversion of funding from the common school fund making it, in their opinion, unconstitutional.

What’s the fix? We could amend Article IX, section 2 of the constitution like this:

The legislature shall provide for a general and uniform system of public schools. The public school system shall include common schools, and such high schools, normal schools, and technical schools as may hereafter be established. But the entire revenue derived from the common school fund and the state tax for common schools shall be exclusively applied to the support of the common schools. The state tax for common schools, when authorized by the legislature, may be used for a limited time to retire debt for

local infrastructure projects.

Whether this exact language would work or not is beside the point; it’s the substance that matters. The fact is that Article 2 as it is currently written is pretty clear: the state tax for common schools—which you see itemized on your property tax bill if you have one—can’t be used for any other purpose. So Article 2 is where the action is, and fixing it would open the door for TIF.

But given the fact that the state is being sued by a group of school advocates who say the state isn’t fully funding education it is highly likely that my amendment would flush out passionate opposition. Why would we take an increment of the state tax for common schools to pay off bonds for sidewalks in Kent or stormwater systems in Issaquah when we’re already not even fully funding education? The opposition would likely argue that TIF would siphon funds away from education—not a popular idea.

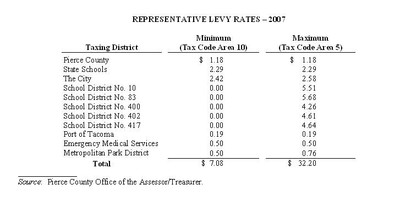

And there is a second big problem. Other junior taxing districts would have to give up a portion of their tax collections as well. To illustrate, here’s a chart showing an example of all the local taxing authorities that collect taxes on property in Pierce County:

Chart from presentation by K and L Gates – Large version here

To make a TIF project work, one or all of these districts would have to give up the incrementally increased portion of their tax collection to pay debt service until the TIF bonds were retired. So add to the chorus of concerned parents and teachers, some axe-wielding fireman and some parks advocates trying to protect their turf and you begin to get the picture of how tough the politics could be.

Now, the Washington legislature has already passed a form of TIF—they call it “TIF Lite”—that allows TIF with agreement from those taxing districts. The legislature also approved a tax credit from the general fund for the portion of state tax for schools. The tax credit allows some portion—up to $5 million statewide—of the general fund to be used this way. So whatever the incremental improvement to the state school tax a project would create comes out of the general fund, not the local school tax. So far, about 9 cities have used this tool. So don’t we have TIF already?

It turns out that the TIF Lite solution doesn’t work very well because it requires agreement from all the different junior taxing districts, and the amount of money available from the state to make up for the schools portion is tiny—only $5 million—which not nearly enough to put together the kind of investment that it took make the Pearl District come together. Remaking a district like the Pearl is a multi-year effort with hundreds of millions of dollars in play. The current TIF legislation doesn’t allow projects at a scale that would create large-scale shifts in land use or big public benefits.

Leaders in the region continue to cite TIF as tool we are going to need to make substantial redevelopment possible in our most populous cities. For example, a white paper on land use written for Seattle’s carbon neutrality planning process found that TIF would be important to creating the compact and affordable communities that are essential to achieving major reductions in carbon emissions. So while there is no easy way politically to get real TIF done in Washington, we shouldn’t just give up. Given the multiple problems of climate, traffic, affordable housing, and bare government coffers, we had better tighten up the ski boots and learn to navigate the double black diamond politics of TIF.

Photo Credit: Photo of Portland’s Pearl District from Flickr Gilbert928’s Photostream

{kind=link}

Comments